How Georgia Gold Export Connects a 3,000-Year Heritage to Global Markets Today

Georgia Gold Export: From Ancient Golden Fleece to $639M in Modern Trade Georgia gold export carries a story that stretches back thousands of years….

Read More

Georgia Gold Export: From Ancient Golden Fleece to $639M in Modern Trade Georgia gold export carries a story that stretches back thousands of years….

Read More

Construction Sector Georgia: 10,495 Permits, $241M Invested and 86% Growth The construction sector Georgia is experiencing rapid and measurable growth. Construction and building —…

Read More

Protein rich hazelnuts are sweet tree nuts that grow in temperate zones and its mainly cultivated in Turkey, which produces about 60% of the world’s…

Read More

Tea is the oldest Chinese culture, known in 1753 by a well-known Swedish botanist Carl Lynne, first described as a scientific name (Thea). Tea is…

Read More

Georgian mandarin is cultivated in Western regions of Georgia, in Adjara, Guria, Samegrelo and Apkhazia. Russia and Ukraine are leading Georgian mandarin export countries,…

Read More

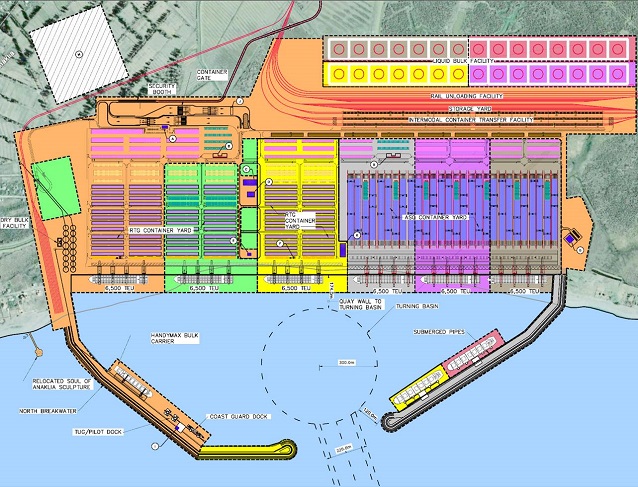

The Port of Anaklia is located on the shortest route from China to Europe, a route that has become a major focal point of Chinese…

Read More

Over the last decade electricity consumption in Georgia has grown largely in line with real GDP growth rate and reached 10.4 TWh in 2015. If…

Read More

An estimated 250,000 rural Georgians benefited from current support, EU announces third phase of assistance worth 230 million GEL 13, December 2017, Tbilisi –…

Read More

On November 15, after three years of technical talks, during the 7th Regional Economic Cooperation Conference on Afghanistan (RECCA-VII) in Ashgabat, Turkmenistan was signed…

Read More

In 5 years, Georgia will offer to the local and international visitors the Enguri River dam, which is planned to become a unique tourist…

Read More